Planning your investments becomes much easier when you know how much wealth your money can create over time. A SIP (Systematic Investment Plan) Calculator helps you estimate the future value of your monthly investments based on the amount you invest, the expected annual return, and the investment duration.

Whether you’re investing ₹500 every month or planning to invest $500, €500, £500, A$500, NZ$500, or C$500 regularly, this calculator gives you an estimate of your investment growth within seconds. It supports multiple currencies and also includes a Lumpsum Calculator, making it a complete investment planning tool for investors across the world.

Unlike manual calculations, a SIP Calculator instantly shows your total investment, estimated returns, maturity amount, and a graphical representation of your investment growth. This helps you compare different investment scenarios, set realistic financial goals, and make smarter decisions without performing complex mathematical calculations.

Whether you’re saving for retirement, your child’s education, buying a house, building an emergency fund, or creating long-term wealth, this calculator provides a quick and reliable estimate to help you stay on track.

Try Our Free SIP Calculator

Investment Calculator

Total Invested

Total Returns

Maturity Amount

Inflation Adjusted Value

Year-wise Growth Table

| Year | Invested Amount | Estimated Value | Estimated Returns |

|---|

What Is SIP?

A Systematic Investment Plan (SIP) is one of the most popular investment methods used in mutual funds. Instead of investing a large amount at one time, SIP allows investors to invest a fixed amount at regular intervals, usually every month.

For example, if you decide to invest ₹5,000 every month into a mutual fund, your money is automatically invested on the selected date every month. Over time, these regular investments help you build wealth through the power of compounding and rupee cost averaging.

SIP is suitable for both beginners and experienced investors because it encourages disciplined investing without requiring a large initial investment.

Unlike traditional savings accounts, SIP investments have the potential to generate higher long-term returns because they are invested in market-linked mutual funds.

Example

Suppose you invest:

- Monthly Investment: ₹5,000

- Expected Return: 12%

- Investment Period: 20 Years

Total Investment:

₹12,00,000

Estimated Wealth:

Approximately ₹49–50 Lakhs

This demonstrates how regular investments combined with compounding can significantly increase your wealth over time.

What Does SIP Stand For?

SIP stands for Systematic Investment Plan.

It is a facility offered by mutual fund companies that allows investors to invest a fixed amount periodically instead of making a one-time investment.

How Does SIP Work?

A SIP works by automatically investing a fixed amount into your selected mutual fund at regular intervals.

Here’s how it works:

- Select a mutual fund.

- Decide your monthly investment amount.

- Choose your investment date.

- The amount is automatically deducted from your bank account.

- Mutual fund units are allotted based on the day’s NAV.

- Continue investing every month.

- Over time, your investment grows through compounding.

Since markets fluctuate daily, sometimes you purchase more units and sometimes fewer units. This strategy is called Rupee Cost Averaging, which helps reduce the impact of market volatility over the long term.

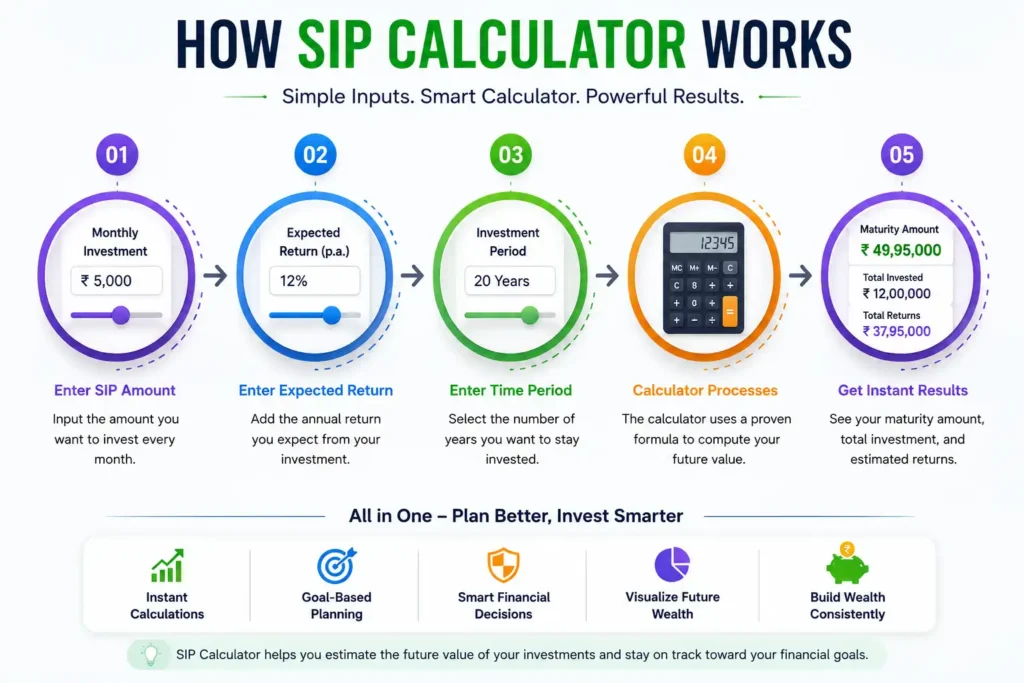

What Is a SIP Calculator?

A SIP Calculator is an online financial planning tool that estimates the future value of your SIP investments.

Instead of manually applying complicated mathematical formulas, the calculator instantly computes your estimated returns based on three simple inputs:

- Monthly Investment

- Expected Annual Return

- Investment Duration

The calculator then displays:

- Total Amount Invested

- Estimated Wealth Created

- Total Profit

- Maturity Value

- Investment Growth Chart

This helps investors compare different investment scenarios before starting their SIP journey.

Why Should You Use a SIP Calculator?

Many people begin investing without knowing how much wealth they can accumulate over time. A SIP Calculator removes the guesswork by providing quick and reliable estimates.

Some key advantages include:

1. Saves Time

Manual SIP calculations are lengthy and complicated. A calculator provides instant results within seconds.

2. Better Financial Planning

Knowing your future investment value helps you plan for major life goals such as retirement, education, buying a house, or building an emergency fund.

3. Easy Goal Planning

You can experiment with different monthly investment amounts and investment durations to determine how much you need to invest to reach your financial target.

4. Compare Multiple Scenarios

For example:

- ₹2,000 for 20 years

- ₹5,000 for 15 years

- ₹10,000 for 10 years

The calculator helps you compare which option aligns best with your financial goals.

5. Helps Beginners

Even first-time investors with no financial background can understand their potential returns using a simple calculator.

How Our SIP Calculator Works

Our calculator uses the standard SIP future value formula to estimate the maturity amount.

It requires only three inputs.

Monthly Investment

This is the amount you invest every month.

Examples include:

- ₹500

- ₹1,000

- ₹2,500

- ₹5,000

- ₹10,000

- ₹20,000

The higher your monthly investment, the greater your potential wealth accumulation over time.

Expected Annual Return

This is the estimated annual return from your mutual fund investment.

Typical assumptions include:

| Investment Type | Expected Annual Return |

|---|---|

| Debt Funds | 6%–8% |

| Hybrid Funds | 8%–10% |

| Large Cap Equity Funds | 10%–12% |

| Flexi Cap Funds | 11%–13% |

| Mid Cap Funds | 12%–15% |

| Small Cap Funds | 13%–16% |

Remember that these are estimates and actual returns may vary depending on market performance.

Investment Duration

This refers to how long you continue your SIP.

Examples:

- 5 Years

- 10 Years

- 15 Years

- 20 Years

- 25 Years

- 30 Years

Longer investment periods generally provide greater benefits because of compounding.

Understanding the Power of Compounding

Compounding is often described as earning returns not only on your original investment but also on the returns already generated.

This creates a snowball effect over time.

Example

Suppose you invest ₹5,000 every month at an expected annual return of 12%.

| Years | Total Invested | Estimated Value |

|---|---|---|

| 5 | ₹3,00,000 | ₹4.1 Lakhs |

| 10 | ₹6,00,000 | ₹11.6 Lakhs |

| 15 | ₹9,00,000 | ₹25 Lakhs |

| 20 | ₹12,00,000 | ₹50 Lakhs |

| 25 | ₹15,00,000 | ₹95 Lakhs |

| 30 | ₹18,00,000 | ₹1.76 Crore |

As the table shows, your wealth grows much faster during the later years because of compounding. This is why starting early and staying invested for the long term can significantly improve your financial outcomes.

Understanding Every Input in the SIP Calculator

To make informed decisions, it is important to understand what each field in the calculator represents and how changing it affects your results.

Monthly Investment

This is the fixed amount you commit to investing every month. Increasing this amount can have a significant impact on your final corpus because every additional contribution also benefits from future compounding.

Expected Return

This is the annual growth rate assumed by the calculator. It is only an estimate and should not be treated as a guaranteed return. Choosing a realistic return assumption helps you create practical financial plans.

Investment Period

This is the number of years you plan to continue investing. Even if your monthly contribution remains the same, extending the investment period often results in much higher wealth creation due to the compounding effect.

Currency Selection

Our calculator supports multiple currencies, including INR, USD, EUR, GBP, AUD, NZD, and CAD. This makes it useful for investors in different countries who want to estimate the future value of their investments using their preferred currency.

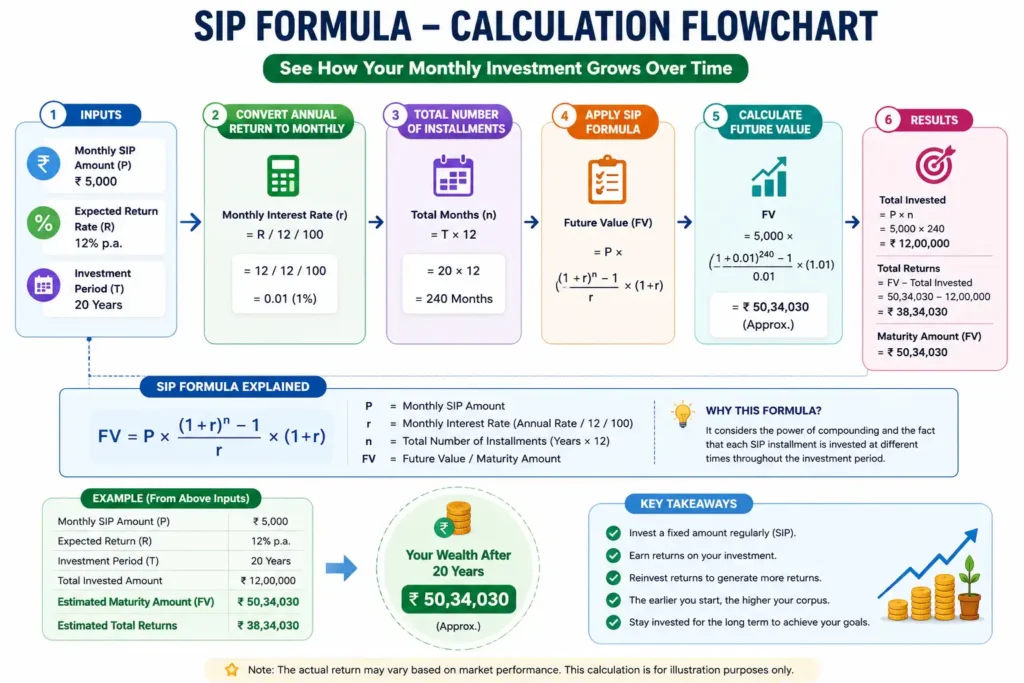

SIP Formula Explained

Understanding how SIP returns are calculated helps you make smarter investment decisions. While our SIP Calculator performs these calculations instantly, knowing the formula behind it gives you a better understanding of how your money grows over time.

Unlike simple interest, SIP investments benefit from compound growth, where you earn returns not only on your original investment but also on the returns accumulated over previous periods. This compounding effect is one of the biggest reasons why SIPs are considered an effective long-term wealth creation tool.

SIP Future Value Formula

The maturity amount of a SIP is calculated using the following formula:

FV = P × [((1 + r)^n − 1) / r] × (1 + r)

Where:

| Symbol | Meaning |

|---|---|

| FV | Future Value (Maturity Amount) |

| P | Monthly SIP Investment |

| r | Monthly Rate of Return (Annual Return ÷ 12 ÷ 100) |

| n | Total Number of Monthly Installments |

Although this formula may appear complex, the calculator performs all calculations automatically in the background.

Understanding the Formula Step by Step

Let’s understand the formula using a practical example.

Example

Monthly SIP: ₹5,000

Expected Return: 12% per year

Investment Duration: 20 years

Step 1: Monthly Return

Annual Return = 12%

Monthly Return

12 ÷ 12 = 1%

Monthly Return = 0.01

Step 2: Total Months

20 Years × 12

= 240 Months

Step 3: Apply Formula

After applying the SIP formula,

Estimated Maturity Value

≈ ₹49.95 Lakhs

Step 4: Calculate Total Investment

₹5,000 × 240

= ₹12,00,000

Step 5: Wealth Created

₹49.95 Lakhs − ₹12 Lakhs

= ₹37.95 Lakhs

Example Calculations

Example 1

| Details | Value |

|---|---|

| Monthly Investment | ₹2,000 |

| Return | 10% |

| Duration | 10 Years |

Results

| Item | Amount |

|---|---|

| Total Investment | ₹2,40,000 |

| Estimated Returns | ₹1,69,000 |

| Maturity Amount | ₹4,09,000 |

Example 2

| Details | Value |

|---|---|

| Monthly Investment | ₹10,000 |

| Return | 12% |

| Duration | 15 Years |

| Item | Amount |

|---|---|

| Total Investment | ₹18,00,000 |

| Estimated Returns | ₹32,50,000 |

| Maturity Amount | ₹50,50,000 |

Example 3

| Details | Value |

|---|---|

| Monthly Investment | ₹20,000 |

| Return | 12% |

| Duration | 25 Years |

| Item | Amount |

|---|---|

| Total Investment | ₹60,00,000 |

| Estimated Returns | ₹2.80 Crore |

| Estimated Corpus | ₹3.40 Crore |

Why Does Investment Duration Matter So Much?

Many beginners focus only on increasing their monthly investment. However, the investment duration has an even bigger impact on long-term wealth.

Consider investing ₹5,000 every month at an expected return of 12%.

| Investment Period | Total Invested | Estimated Corpus |

|---|---|---|

| 5 Years | ₹3,00,000 | ₹4.1 Lakhs |

| 10 Years | ₹6,00,000 | ₹11.6 Lakhs |

| 15 Years | ₹9,00,000 | ₹25 Lakhs |

| 20 Years | ₹12 Lakhs | ₹50 Lakhs |

| 25 Years | ₹15 Lakhs | ₹95 Lakhs |

| 30 Years | ₹18 Lakhs | ₹1.76 Crore |

Notice how the investment grows much faster during the later years. This is the power of compounding at work.

Why Expected Returns Are Only Estimates

One of the most common misconceptions is that the calculator predicts your exact future returns.

In reality, the calculator uses an assumed annual return. Mutual funds invest in market-linked securities, and their performance can vary from year to year.

For example:

| Year | Actual Return |

|---|---|

| Year 1 | 8% |

| Year 2 | 14% |

| Year 3 | -5% |

| Year 4 | 20% |

| Year 5 | 11% |

The SIP Calculator simplifies this by assuming an average annual return over the investment period.

This makes it an excellent planning tool but not a guarantee of future performance.

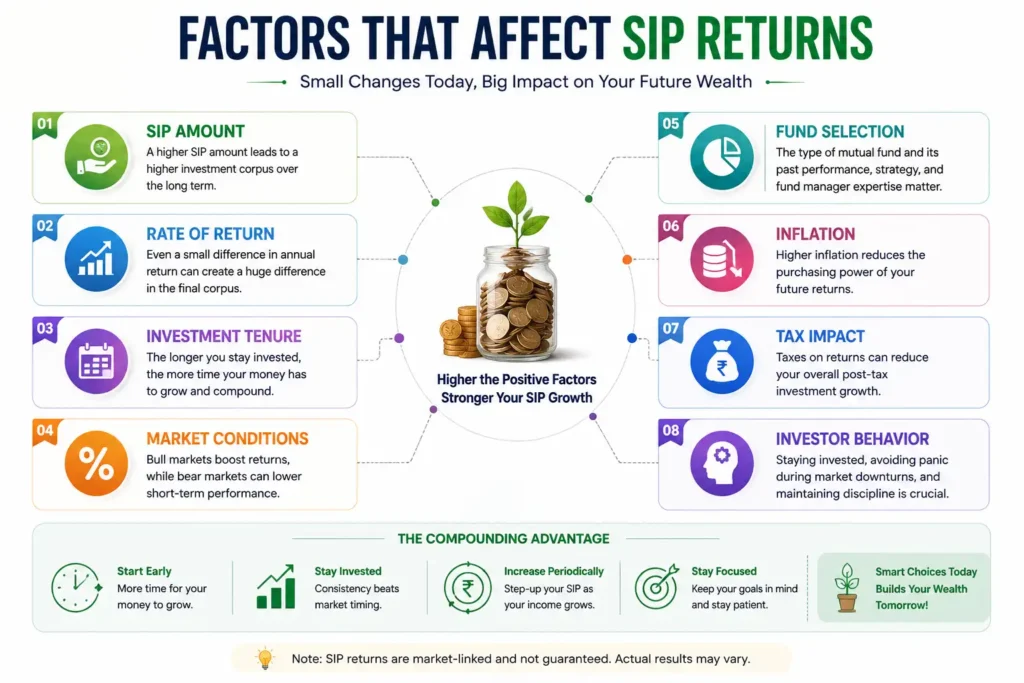

Factors That Affect SIP Returns

Several factors influence the actual returns generated by your SIP investments.

1. Market Performance

Equity mutual funds are directly linked to stock market movements. During bull markets, returns may exceed expectations, while bear markets may temporarily reduce portfolio value.

2. Investment Duration

Longer investment horizons generally reduce the impact of short-term market volatility and increase the benefits of compounding.

3. Fund Selection

Not all mutual funds deliver the same returns. Choosing funds with a strong long-term track record, experienced fund managers, and consistent performance can improve outcomes.

4. Expense Ratio

Mutual funds charge a small annual fee known as the expense ratio. Lower expense ratios can help investors retain more of their returns over time.

5. Market Timing

Although SIPs reduce the need to time the market, starting your investment early allows more time for compounding to work.

6. Increasing Your SIP

Regularly increasing your SIP amount as your income grows can significantly enhance your final corpus.

SIP vs Lumpsum Investment

Both SIP and Lumpsum are popular ways to invest in mutual funds. The right choice depends on your financial situation, income pattern, investment goals, and risk tolerance.

A SIP spreads your investment over time through regular monthly contributions, while a Lumpsum investment involves investing a large amount at once.

Let’s compare them in detail.

| Feature | SIP | Lumpsum |

|---|---|---|

| Investment Style | Monthly | One Time |

| Initial Capital | Low | High |

| Market Timing | Not Required | Important |

| Suitable for Salaried Individuals | Yes | Limited |

| Suitable for Bonus/Inheritance | No | Yes |

| Rupee Cost Averaging | Yes | No |

| Investment Discipline | High | Moderate |

| Risk During Market Fall | Lower | Higher |

| Flexibility | High | Moderate |

What Is a SIP?

A SIP allows you to invest a fixed amount every month.

Example:

₹5,000 every month for 20 years.

Advantages include:

- Affordable

- Automatic investing

- Better financial discipline

- Reduces emotional investing

- Ideal for long-term wealth creation

What Is a Lumpsum Investment?

A lumpsum investment means investing the entire amount at once.

Example:

Investing ₹10 Lakhs today in a mutual fund.

This approach is commonly chosen when an investor receives:

- Annual bonus

- Inheritance

- Sale proceeds from property

- Retirement benefits

- Business profits

If the investment is made when markets are reasonably valued and held for the long term, it can generate substantial returns. However, it also exposes the investor to higher short-term market risk.

SIP vs Lumpsum: Example Comparison

Suppose an investor has ₹12,00,000 available.

Option 1: SIP

Monthly Investment: ₹50,000

Duration: 24 Months

Expected Return: 12%

The investment is spread over two years, reducing the impact of market fluctuations.

Option 2: Lumpsum

Invest ₹12,00,000 immediately.

If the market rises after investing, the investor benefits from the full amount being invested from day one.

If the market declines sharply, the portfolio may experience larger short-term losses.

When Should You Choose SIP?

A SIP is generally more suitable if:

- You receive a monthly salary.

- You are new to investing.

- You want to build long-term wealth.

- You prefer investing small amounts regularly.

- You want to avoid worrying about market timing.

- You are investing for goals such as retirement, education, or buying a home.

When Should You Choose Lumpsum?

A lumpsum investment may be appropriate if:

- You have a large amount of idle money.

- You receive an annual bonus or inheritance.

- You have already built an emergency fund.

- You have a long investment horizon.

- You understand market volatility and can tolerate short-term fluctuations.

Can You Use Both SIP and Lumpsum?

Yes. Many experienced investors combine both approaches.

For example:

- Invest a bonus of ₹5,00,000 as a lumpsum.

- Continue a monthly SIP of ₹10,000.

This strategy allows you to put excess funds to work immediately while maintaining disciplined, regular investing for the future.

Which Is Better: SIP or Lumpsum?

There is no universal answer. The better option depends on your financial situation and goals.

For most salaried individuals and first-time investors, SIP offers several advantages, including affordability, reduced market timing risk, and disciplined investing.

Lumpsum investing can be more rewarding when you have a substantial amount available and are comfortable with market fluctuations over the long term.

Many investors find that using a combination of both strategies provides the right balance between opportunity and consistency.

Top Benefits of Investing Through SIP

Systematic Investment Plans (SIPs) have become one of the most popular investment methods for building long-term wealth. Whether you are a beginner investing your first ₹500 or an experienced investor contributing ₹50,000 every month, SIPs offer several advantages that help you achieve your financial goals in a disciplined and efficient manner.

Unlike one-time investments, SIPs allow you to invest a fixed amount regularly, making wealth creation more accessible and less dependent on market timing. Let’s explore the key benefits in detail.

1. Power of Compounding

Compounding is one of the biggest reasons why SIPs are recommended for long-term investors. It means earning returns not only on your original investment but also on the returns accumulated over time.

The longer you stay invested, the greater the impact of compounding.

Example

Suppose you invest ₹5,000 every month at an expected annual return of 12%.

| Investment Period | Total Invested | Estimated Corpus |

|---|---|---|

| 10 Years | ₹6,00,000 | ₹11.6 Lakhs |

| 20 Years | ₹12,00,000 | ₹50 Lakhs |

| 30 Years | ₹18,00,000 | ₹1.76 Crore |

Although your monthly investment remains the same, the wealth created increases dramatically over longer periods because each year’s gains begin generating additional gains.

Key Takeaway: Start early. Time in the market is usually more powerful than trying to time the market.

2. Rupee Cost Averaging

Markets rise and fall regularly. Investing a fixed amount every month allows you to buy more mutual fund units when prices are low and fewer units when prices are high.

This process is known as Rupee Cost Averaging.

Example

| Month | NAV | Monthly SIP | Units Purchased |

|---|---|---|---|

| January | ₹20 | ₹5,000 | 250 |

| February | ₹18 | ₹5,000 | 277.78 |

| March | ₹16 | ₹5,000 | 312.50 |

| April | ₹22 | ₹5,000 | 227.27 |

Instead of worrying about market volatility, SIP automatically averages your purchase cost over time.

3. Affordable Investment Option

One of the biggest advantages of SIP is that you don’t need a large amount to start investing.

Many mutual funds allow investors to begin with as little as:

- ₹100

- ₹500

- ₹1,000

This makes investing accessible to:

- Students

- Young professionals

- Salaried employees

- Freelancers

- Small business owners

Even small monthly contributions can grow into a substantial corpus over the long term.

4. Builds Financial Discipline

Successful investing is often more about consistency than making large investments.

SIP promotes disciplined investing by automatically deducting your chosen amount every month. This helps you:

- Develop a regular saving habit.

- Avoid skipping investments.

- Stay committed to your financial goals.

- Reduce impulsive spending.

Automatic investments remove emotional decision-making and encourage long-term consistency.

5. No Need to Time the Market

Predicting the perfect time to invest is extremely difficult, even for experienced investors.

With SIP, you invest regularly regardless of whether the market is rising or falling.

This approach helps reduce the stress of market timing and ensures that your money remains invested throughout different market cycles.

Remember: Consistent investing over the long term generally produces better results than waiting for the “perfect” entry point.

6. Flexibility

SIPs offer a high level of flexibility, allowing investors to tailor their investments according to their financial situation.

You can:

- Increase your monthly SIP.

- Reduce your SIP amount (subject to fund rules).

- Pause SIPs temporarily.

- Stop SIPs without penalties in most open-ended schemes.

- Start additional SIPs in different funds.

This flexibility makes SIPs suitable for changing financial needs over time.

7. Goal-Based Investing

Every financial goal has a different investment requirement.

SIPs make it easier to invest specifically for goals such as:

- Child’s education

- Marriage

- Retirement

- Home purchase

- Dream vacation

- Car purchase

- Emergency fund

- Wealth creation

By calculating the required monthly investment, you can align your SIP with your target amount and timeline.

Example

| Financial Goal | Target Amount | Investment Horizon |

|---|---|---|

| Child Education | ₹30 Lakhs | 15 Years |

| Retirement | ₹3 Crore | 30 Years |

| Home Down Payment | ₹25 Lakhs | 10 Years |

| Car Purchase | ₹10 Lakhs | 5 Years |

8. Suitable for All Income Levels

Whether you earn ₹25,000 or ₹2,50,000 per month, SIP can fit into your budget.

For example:

| Monthly Income | Suggested SIP |

|---|---|

| ₹25,000 | ₹2,000–₹3,000 |

| ₹50,000 | ₹5,000–₹8,000 |

| ₹1,00,000 | ₹10,000–₹20,000 |

| ₹2,00,000 | ₹20,000–₹50,000 |

The key is to invest consistently and gradually increase your SIP as your income grows.

9. Potential to Beat Inflation

Inflation gradually reduces the purchasing power of money.

For example, an item costing ₹1,00,000 today may cost significantly more after 20 years.

Keeping your money in a low-interest savings account may not keep pace with inflation.

Historically, equity-oriented mutual funds have delivered returns that have often outpaced inflation over long investment horizons, helping investors preserve and grow their purchasing power.

10. Long-Term Wealth Creation

SIP is not designed to generate quick profits. Instead, it is a long-term wealth-building strategy.

Investors who remain disciplined through market ups and downs are more likely to benefit from:

- Compounding

- Rupee cost averaging

- Long-term market growth

- Lower emotional decision-making

Over decades, even modest monthly investments can grow into a substantial financial corpus.

Types of SIP

Not all SIPs work the same way. Mutual fund companies offer different SIP options to suit various investment needs, income patterns, and financial goals.

Understanding these types can help you choose the right investment strategy.

1. Regular SIP

A Regular SIP is the most common type of SIP.

You invest a fixed amount at regular intervals, usually every month.

Best For

- Salaried employees

- First-time investors

- Long-term wealth creation

Example

Monthly Investment: ₹5,000

Duration: 20 Years

The amount remains unchanged throughout the investment period.

Advantages

- Easy to start

- Highly disciplined

- Automatic investments

- Simple to manage

2. Step-Up SIP (Top-Up SIP)

A Step-Up SIP allows you to increase your SIP amount periodically, usually every year.

For example:

Year 1: ₹5,000/month

Year 2: ₹5,500/month

Year 3: ₹6,000/month

This strategy helps your investments grow alongside your income.

Benefits

- Higher long-term wealth creation

- Keeps pace with salary increments

- Better inflation management

- Ideal for young professionals

Example of Step-Up SIP

| Year | Monthly SIP |

|---|---|

| 1 | ₹5,000 |

| 2 | ₹5,500 |

| 3 | ₹6,000 |

| 4 | ₹6,500 |

| 5 | ₹7,000 |

A modest annual increase can significantly boost your final corpus over the long term.

3. Flexible SIP

Flexible SIP allows investors to change their monthly investment amount based on their financial circumstances.

For example:

- Increase investments during high-income months.

- Reduce investments during periods of financial strain.

Best For

- Freelancers

- Business owners

- Individuals with irregular income

4. Perpetual SIP

A Perpetual SIP has no predefined end date.

Instead of selecting a fixed duration, the SIP continues until the investor chooses to stop it.

Benefits

- No need to renew SIPs.

- Suitable for retirement planning.

- Encourages continuous investing.

5. Trigger SIP

Trigger SIP allows investments to be activated automatically when specific market conditions are met.

Examples include:

- Market falls by 10%.

- NAV reaches a target level.

- Index crosses a specific value.

This type is generally more suitable for experienced investors who actively monitor the market.

6. Multi SIP

A Multi SIP allows investors to invest in multiple mutual fund schemes through a single SIP mandate.

Benefits

- Better diversification.

- Easier portfolio management.

- Automatic asset allocation.

- Reduced paperwork.

7. Value SIP

A Value SIP adjusts your investment amount based on market valuations.

When markets decline, you invest more.

When markets rise significantly, you invest less.

This strategy aims to accumulate more units during market corrections.

8. ELSS SIP

An ELSS (Equity Linked Savings Scheme) SIP combines regular investing with tax-saving benefits under applicable tax laws.

Key Features

- Tax-saving mutual fund.

- Equity-oriented investment.

- Three-year lock-in for each installment.

- Suitable for long-term investors seeking both tax efficiency and wealth creation.

9. Smart SIP

Some investment platforms offer Smart SIPs that use predefined rules or algorithms to adjust investments based on market conditions or investor preferences.

These may include:

- Market valuation indicators.

- Asset allocation models.

- Automatic rebalancing.

- Dynamic investment adjustments.

Which Type of SIP Should You Choose?

| SIP Type | Best For | Risk Level |

|---|---|---|

| Regular SIP | Beginners | Low |

| Step-Up SIP | Salaried Professionals | Low |

| Flexible SIP | Freelancers & Business Owners | Medium |

| Perpetual SIP | Long-Term Investors | Low |

| Trigger SIP | Experienced Investors | High |

| Multi SIP | Diversification | Medium |

| Value SIP | Advanced Investors | Medium |

| ELSS SIP | Tax Saving | Medium |

| Smart SIP | Goal-Based Investors | Medium |

Expert Tip

For most investors, a Step-Up SIP is often one of the most effective strategies. Increasing your monthly investment by just 10% every year can potentially result in a much larger retirement corpus compared to maintaining a fixed SIP amount throughout your investment journey.

SIP Return Examples

One of the biggest advantages of using a SIP Calculator is that it helps you estimate how your investments may grow over time. By adjusting the monthly investment amount, expected annual return, and investment duration, you can compare different scenarios and choose a plan that aligns with your financial goals.

The following examples are based on assumed annual returns. Actual returns may vary depending on market conditions and the performance of the mutual fund you choose.

SIP Growth at 8% Annual Return

Monthly SIP: ₹1,000

| Investment Period | Total Invested | Estimated Maturity | Estimated Returns |

|---|---|---|---|

| 5 Years | ₹60,000 | ₹73,000 | ₹13,000 |

| 10 Years | ₹1,20,000 | ₹1.83 Lakhs | ₹63,000 |

| 15 Years | ₹1,80,000 | ₹3.46 Lakhs | ₹1.66 Lakhs |

| 20 Years | ₹2,40,000 | ₹5.89 Lakhs | ₹3.49 Lakhs |

| 25 Years | ₹3,00,000 | ₹9.51 Lakhs | ₹6.51 Lakhs |

| 30 Years | ₹3,60,000 | ₹13.80 Lakhs | ₹10.20 Lakhs |

Monthly SIP: ₹5,000

| Investment Period | Total Invested | Estimated Maturity |

|---|---|---|

| 5 Years | ₹3 Lakhs | ₹3.65 Lakhs |

| 10 Years | ₹6 Lakhs | ₹9.15 Lakhs |

| 15 Years | ₹9 Lakhs | ₹17.30 Lakhs |

| 20 Years | ₹12 Lakhs | ₹29.45 Lakhs |

| 25 Years | ₹15 Lakhs | ₹47.55 Lakhs |

| 30 Years | ₹18 Lakhs | ₹69 Lakhs |

Monthly SIP: ₹10,000

| Investment Period | Total Invested | Estimated Maturity |

|---|---|---|

| 5 Years | ₹6 Lakhs | ₹7.30 Lakhs |

| 10 Years | ₹12 Lakhs | ₹18.30 Lakhs |

| 15 Years | ₹18 Lakhs | ₹34.60 Lakhs |

| 20 Years | ₹24 Lakhs | ₹58.90 Lakhs |

| 25 Years | ₹30 Lakhs | ₹95 Lakhs |

| 30 Years | ₹36 Lakhs | ₹1.38 Crore |

SIP Growth at 10% Annual Return

Monthly SIP: ₹5,000

| Investment Period | Total Invested | Estimated Corpus |

|---|---|---|

| 5 Years | ₹3 Lakhs | ₹3.90 Lakhs |

| 10 Years | ₹6 Lakhs | ₹10.30 Lakhs |

| 15 Years | ₹9 Lakhs | ₹20.70 Lakhs |

| 20 Years | ₹12 Lakhs | ₹37.90 Lakhs |

| 25 Years | ₹15 Lakhs | ₹65 Lakhs |

| 30 Years | ₹18 Lakhs | ₹1.13 Crore |

SIP Growth at 12% Annual Return

This is one of the most commonly used assumptions for equity mutual funds over the long term.

Monthly SIP: ₹500

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹30,000 | ₹41,000 |

| 10 | ₹60,000 | ₹1.16 Lakhs |

| 15 | ₹90,000 | ₹2.50 Lakhs |

| 20 | ₹1.20 Lakhs | ₹5 Lakhs |

| 25 | ₹1.50 Lakhs | ₹9.50 Lakhs |

| 30 | ₹1.80 Lakhs | ₹17.60 Lakhs |

Monthly SIP: ₹1,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹60,000 | ₹82,000 |

| 10 | ₹1.20 Lakhs | ₹2.32 Lakhs |

| 15 | ₹1.80 Lakhs | ₹5 Lakhs |

| 20 | ₹2.40 Lakhs | ₹10 Lakhs |

| 25 | ₹3 Lakhs | ₹19 Lakhs |

| 30 | ₹3.60 Lakhs | ₹35 Lakhs |

Monthly SIP: ₹2,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹1.20 Lakhs | ₹1.64 Lakhs |

| 10 | ₹2.40 Lakhs | ₹4.64 Lakhs |

| 15 | ₹3.60 Lakhs | ₹10 Lakhs |

| 20 | ₹4.80 Lakhs | ₹20 Lakhs |

| 25 | ₹6 Lakhs | ₹38 Lakhs |

| 30 | ₹7.20 Lakhs | ₹70 Lakhs |

Monthly SIP: ₹5,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹3 Lakhs | ₹4.10 Lakhs |

| 10 | ₹6 Lakhs | ₹11.60 Lakhs |

| 15 | ₹9 Lakhs | ₹25 Lakhs |

| 20 | ₹12 Lakhs | ₹50 Lakhs |

| 25 | ₹15 Lakhs | ₹95 Lakhs |

| 30 | ₹18 Lakhs | ₹1.76 Crore |

Monthly SIP: ₹10,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹6 Lakhs | ₹8.20 Lakhs |

| 10 | ₹12 Lakhs | ₹23.20 Lakhs |

| 15 | ₹18 Lakhs | ₹50 Lakhs |

| 20 | ₹24 Lakhs | ₹1 Crore |

| 25 | ₹30 Lakhs | ₹1.90 Crore |

| 30 | ₹36 Lakhs | ₹3.52 Crore |

Monthly SIP: ₹20,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹12 Lakhs | ₹16.40 Lakhs |

| 10 | ₹24 Lakhs | ₹46 Lakhs |

| 15 | ₹36 Lakhs | ₹1 Crore |

| 20 | ₹48 Lakhs | ₹2 Crore |

| 25 | ₹60 Lakhs | ₹3.80 Crore |

| 30 | ₹72 Lakhs | ₹7.04 Crore |

Monthly SIP: ₹50,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹30 Lakhs | ₹41 Lakhs |

| 10 | ₹60 Lakhs | ₹1.16 Crore |

| 15 | ₹90 Lakhs | ₹2.50 Crore |

| 20 | ₹1.20 Crore | ₹5 Crore |

| 25 | ₹1.50 Crore | ₹9.50 Crore |

| 30 | ₹1.80 Crore | ₹17.60 Crore |

Monthly SIP: ₹1,00,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹60 Lakhs | ₹82 Lakhs |

| 10 | ₹1.20 Crore | ₹2.32 Crore |

| 15 | ₹1.80 Crore | ₹5 Crore |

| 20 | ₹2.40 Crore | ₹10 Crore |

| 25 | ₹3 Crore | ₹19 Crore |

| 30 | ₹3.60 Crore | ₹35.20 Crore |

SIP Growth at 15% Annual Return

A 15% annual return assumption is generally associated with higher-risk equity investments over long periods and should not be considered guaranteed.

Monthly SIP: ₹5,000

| Years | Total Investment | Estimated Corpus |

|---|---|---|

| 5 | ₹3 Lakhs | ₹4.50 Lakhs |

| 10 | ₹6 Lakhs | ₹14 Lakhs |

| 15 | ₹9 Lakhs | ₹36 Lakhs |

| 20 | ₹12 Lakhs | ₹76 Lakhs |

| 25 | ₹15 Lakhs | ₹1.55 Crore |

| 30 | ₹18 Lakhs | ₹3.05 Crore |

How Much SIP Do You Need to Reach Your Financial Goal?

A SIP Calculator is especially useful for goal-based investing. Instead of investing randomly, you can estimate how much you need to invest each month to achieve a specific target.

Below are examples assuming a 12% annual return.

| Financial Goal | Investment Horizon | Approximate Monthly SIP |

|---|---|---|

| ₹10 Lakhs | 10 Years | ₹4,300 |

| ₹25 Lakhs | 15 Years | ₹5,000 |

| ₹50 Lakhs | 20 Years | ₹5,000 |

| ₹1 Crore | 20 Years | ₹10,000 |

| ₹2 Crore | 20 Years | ₹20,000 |

| ₹5 Crore | 25 Years | ₹26,000–₹30,000 |

| ₹10 Crore | 30 Years | ₹28,000–₹32,000 |

Note: These figures are approximate and depend on actual investment returns.

Goal-Based SIP Planning

One of the biggest mistakes investors make is investing without a specific objective. A goal-based investment approach helps you determine the right SIP amount, investment period, and risk level based on what you want to achieve.

1. Child’s Education

Higher education costs continue to rise every year. Starting a SIP early can help you build the required corpus without financial stress.

Example

- Current Child’s Age: 5 Years

- Education After: 13 Years

- Estimated Future Cost: ₹30 Lakhs

A monthly SIP invested consistently over this period can help you reach your target.

2. Retirement Planning

Retirement planning is one of the most common reasons people start SIPs.

If you begin investing in your 30s and continue until retirement, you benefit from decades of compounding.

Example Goal

- Retirement Corpus: ₹5 Crore

- Investment Horizon: 30 Years

A disciplined SIP strategy, especially with annual step-ups, can make this goal more achievable.

3. Buying a House

Whether you’re planning for a down payment or purchasing a home outright, a SIP can help you accumulate funds gradually.

Example

- Target Down Payment: ₹25 Lakhs

- Time Available: 10 Years

Estimate the required monthly SIP using the calculator and review your plan periodically.

4. Buying a Car

If you plan to buy a car within the next five to seven years, investing through SIPs may provide better growth potential than simply saving in a traditional bank account, depending on your risk tolerance.

5. Dream Vacation

International vacations often require substantial savings. Instead of relying on credit, you can build a travel fund through regular monthly investments.

6. Emergency Fund

While emergency funds are often kept in liquid or low-risk instruments, a separate SIP for medium-term emergency planning can complement your overall financial strategy.

7. Wealth Creation

Some investors don’t have a specific purchase in mind—they simply want to build long-term wealth. SIPs are well-suited for this purpose because they encourage consistency and harness the power of compounding over many years.

Expert Tip

Whenever possible, review your financial goals every year and consider increasing your SIP amount as your income grows. Even a modest annual increase can have a significant impact on your long-term investment corpus.

SIP vs Fixed Deposit (FD)

Systematic Investment Plans and Fixed Deposits are two of the most popular investment options, but they serve different purposes. While Fixed Deposits focus on capital preservation and guaranteed returns, SIPs are designed for long-term wealth creation through market-linked mutual funds.

If your primary goal is safety and predictable income, a Fixed Deposit may be suitable. However, if you want to grow your wealth over the long term and beat inflation, SIPs often have greater growth potential.

| Feature | SIP | Fixed Deposit |

|---|---|---|

| Risk | Market Linked | Very Low |

| Expected Returns | 10%–15% (Historical, Not Guaranteed) | 5%–8% |

| Wealth Creation Potential | High | Moderate |

| Inflation Protection | Better Over Long Term | Limited |

| Liquidity | High (Subject to Fund Rules) | Penalty on Early Withdrawal |

| Tax Efficiency | Depends on Fund Type | Interest Fully Taxable |

Who Should Choose SIP?

- Investors with a long-term horizon.

- People planning for retirement.

- Wealth creation.

- Child education planning.

- Home purchase planning.

Who Should Choose FD?

- Senior citizens.

- Short-term financial goals.

- Emergency fund.

- Conservative investors.

For many investors, using both SIPs and FDs together provides a balance between growth and stability.

SIP vs Public Provident Fund (PPF)

PPF is a government-backed savings scheme designed for long-term savings with tax benefits. SIPs, on the other hand, invest in mutual funds and offer market-linked returns.

| Feature | SIP | PPF |

|---|---|---|

| Returns | Market Linked | Government Declared |

| Lock-in | No Mandatory Lock-in (Except ELSS) | 15 Years |

| Liquidity | High | Limited |

| Tax Benefits | ELSS Only | Yes |

| Wealth Creation | Higher Potential | Moderate |

| Inflation Beating | Better | Moderate |

PPF is suitable for conservative investors, while SIPs are generally better for long-term wealth accumulation.

SIP vs Recurring Deposit (RD)

Recurring Deposits encourage monthly savings just like SIPs. However, the money is deposited in a bank instead of mutual funds.

| Feature | SIP | RD |

|---|---|---|

| Investment Type | Mutual Fund | Bank Deposit |

| Monthly Investment | Yes | Yes |

| Returns | Market Linked | Fixed |

| Inflation Protection | Better | Limited |

| Wealth Creation | High | Moderate |

| Risk | Moderate | Low |

If your objective is long-term wealth creation, SIPs generally offer better growth potential. If safety is your priority, an RD may be more appropriate.

SIP vs Stocks

Both SIPs and direct stock investments help investors participate in equity markets.

However, they require different levels of knowledge.

| Feature | SIP | Stocks |

|---|---|---|

| Professional Management | Yes | No |

| Diversification | High | Depends on Investor |

| Research Required | Low | High |

| Risk | Moderate | High |

| Suitable for Beginners | Yes | Not Always |

Direct stock investing requires continuous monitoring, while SIPs provide diversification through professionally managed mutual funds.

SIP vs Gold

Gold has traditionally been viewed as a safe-haven asset.

However, it generally serves a different purpose than equity mutual funds.

| Feature | SIP | Gold |

|---|---|---|

| Wealth Creation | High Potential | Moderate |

| Regular Investment | Yes | Yes |

| Inflation Hedge | Good | Good |

| Long-Term Returns | Historically Higher (Equity Funds) | Moderate |

| Volatility | Moderate | Moderate |

Many financial planners recommend holding both gold and equity investments for better diversification.

SIP vs Real Estate

Real estate can generate long-term appreciation, but it requires a significant initial investment.

| Feature | SIP | Real Estate |

|---|---|---|

| Initial Investment | Very Low | Very High |

| Liquidity | High | Low |

| Diversification | Easy | Difficult |

| Maintenance | None | Required |

| Transaction Costs | Very Low | High |

SIPs provide greater flexibility and liquidity, whereas real estate may suit investors looking for physical assets and rental income.

SIP vs National Pension System (NPS)

NPS is specifically designed for retirement planning, whereas SIPs can be used for any financial goal.

| Feature | SIP | NPS |

|---|---|---|

| Retirement Focus | Optional | Primary Objective |

| Tax Benefits | ELSS Only | Available Under Applicable Rules |

| Lock-in | Minimal | Until Retirement (Subject to Rules) |

| Flexibility | High | Moderate |

| Liquidity | High | Limited |

Many investors combine SIPs and NPS to balance retirement planning with broader wealth creation goals.

SIP vs Cryptocurrency

Cryptocurrencies are highly volatile digital assets.

Compared to cryptocurrencies, mutual fund SIPs generally provide a more diversified and professionally managed investment approach.

| Feature | SIP | Cryptocurrency |

|---|---|---|

| Regulation | Regulated Mutual Funds | Varies by Jurisdiction |

| Volatility | Moderate | Very High |

| Diversification | High | Low |

| Long-Term Planning | Suitable | Highly Uncertain |

| Risk Level | Moderate | Very High |

Investors considering cryptocurrencies should understand the associated risks and avoid allocating funds they cannot afford to lose.

Which Investment Option Is Best?

There is no single investment option that is ideal for everyone.

The best choice depends on your:

- Financial goals

- Risk tolerance

- Investment horizon

- Income stability

- Liquidity needs

A diversified portfolio may include multiple asset classes rather than relying on a single investment product.

| Financial Goal | Recommended Investment |

|---|---|

| Retirement | SIP + NPS |

| Emergency Fund | Savings Account + Liquid Fund + FD |

| Tax Saving | ELSS SIP + PPF |

| Child Education | Equity SIP |

| Home Purchase | SIP + Debt Funds |

| Capital Protection | FD + PPF |

| Wealth Creation | Equity SIP |

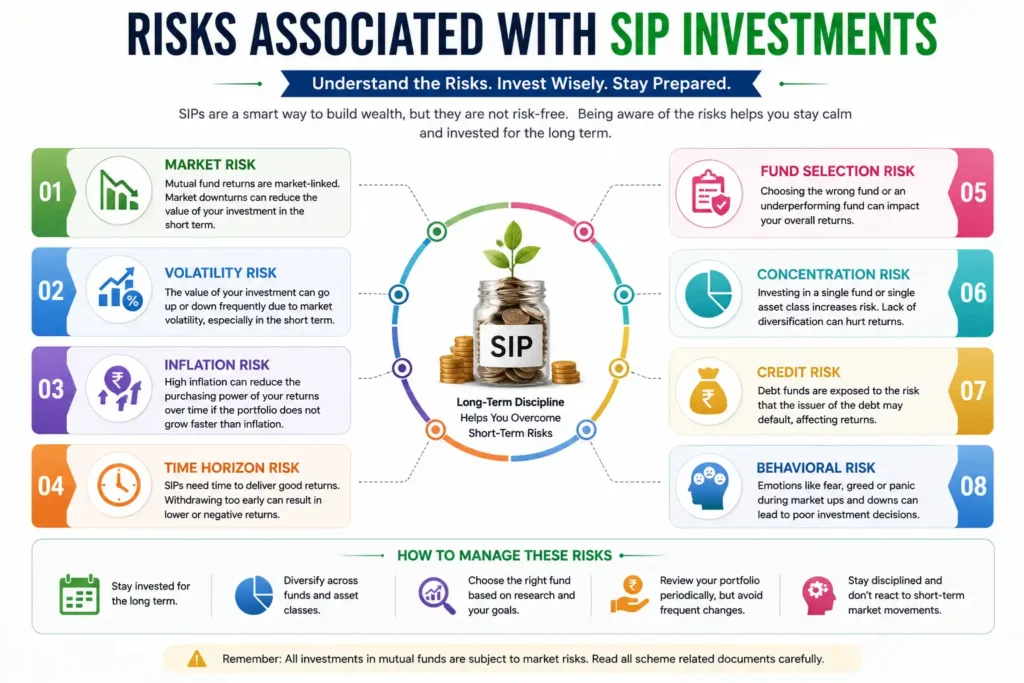

Risks Associated with SIP Investments

Although SIPs are one of the most effective long-term investment strategies, they are not risk-free. Understanding these risks can help investors make informed decisions and avoid unrealistic expectations.

Market Risk

Mutual funds invest in financial markets, which are influenced by economic conditions, corporate earnings, interest rates, and global events.

When markets decline, the value of your investment may also fall temporarily.

However, long-term investors often benefit from market recoveries by continuing their SIPs during downturns.

Volatility Risk

Short-term market fluctuations are common in equity investments.

A portfolio may experience periods of significant gains as well as temporary losses.

Investors should avoid making emotional decisions based on short-term performance.

Inflation Risk

Although SIPs have historically outperformed inflation over long periods, there is no guarantee that future returns will always exceed inflation.

Choosing an appropriate asset allocation is important for managing this risk.

Fund Performance Risk

Not all mutual funds perform equally.

Factors affecting performance include:

- Fund manager decisions.

- Investment strategy.

- Expense ratio.

- Sector allocation.

- Market conditions.

Investors should review their fund’s performance periodically rather than selecting funds based solely on recent returns.

Liquidity Risk

Most open-ended mutual funds allow investors to redeem units at any time. However, some categories may have exit loads or lock-in periods, such as ELSS funds.

Understanding the redemption rules before investing is important.

Interest Rate Risk

Debt mutual funds may be affected by changes in interest rates.

When interest rates rise, the value of certain debt securities can decline.

Investors should choose debt funds that align with their investment horizon and risk profile.

Credit Risk

Debt mutual funds invest in bonds issued by governments and companies.

If an issuer defaults on its obligations or experiences financial difficulties, the fund’s performance may be affected.

High-quality debt funds generally have lower credit risk.

Behavioural Risk

One of the biggest risks to long-term investing is investor behaviour.

Common mistakes include:

- Stopping SIPs during market corrections.

- Redeeming investments after temporary declines.

- Chasing recently high-performing funds.

- Frequently switching between funds.

- Investing without a financial goal.

Maintaining discipline is often more important than trying to predict market movements.

How to Reduce SIP Investment Risks

You cannot eliminate market risk entirely, but you can manage it through prudent investment practices.

Consider the following strategies:

- Invest for the long term.

- Diversify across different fund categories.

- Increase SIPs gradually as income grows.

- Avoid reacting to short-term market movements.

- Review your portfolio annually.

- Align investments with specific financial goals.

- Maintain an emergency fund separate from your investments.

- Consult a qualified financial adviser if needed.

Expert Insights for Long-Term SIP Investors

Successful SIP investing is based on consistency rather than perfection.

Many investors achieve better outcomes by:

- Starting early.

- Remaining invested through market cycles.

- Increasing SIP contributions periodically.

- Staying focused on long-term goals instead of short-term market noise.

- Diversifying investments across appropriate asset classes.

A disciplined investment approach combined with realistic expectations and periodic portfolio reviews can significantly improve the likelihood of achieving long-term financial goals.

Common SIP Mistakes Investors Should Avoid

A SIP is one of the easiest ways to build wealth, but even the best investment strategy can produce disappointing results if common mistakes are made. Understanding these pitfalls can help you stay disciplined and improve your long-term outcomes.

1. Starting Too Late

One of the biggest mistakes is delaying investments.

Many people wait until they have a higher salary or a larger amount to invest. However, time plays a much bigger role in wealth creation than the size of the monthly investment.

Example

Investor A starts investing ₹5,000 per month at age 25 for 30 years.

Investor B starts investing ₹10,000 per month at age 40 for 15 years.

Despite investing half the monthly amount, Investor A may accumulate a larger corpus because of the extra years of compounding.

Lesson: Start as early as possible, even if you can invest only a small amount.

2. Stopping SIP During Market Corrections

Many investors panic when markets decline and stop their SIPs.

Ironically, market corrections are often one of the best times to continue investing because you purchase more units at lower prices.

When the market eventually recovers, these additional units contribute significantly to your portfolio growth.

What You Should Do

- Continue your SIP.

- Avoid checking your portfolio daily.

- Focus on long-term goals.

3. Expecting Guaranteed Returns

A SIP is a method of investing, not a guaranteed-return product.

Your returns depend on:

- Market performance

- Mutual fund selection

- Investment duration

- Economic conditions

Avoid believing advertisements or social media claims promising fixed or guaranteed returns from equity mutual funds.

4. Choosing Funds Based Only on Recent Performance

Many investors select a mutual fund simply because it delivered the highest returns over the past year.

This approach can be misleading.

Instead, evaluate:

- Five- and ten-year performance

- Consistency across market cycles

- Expense ratio

- Fund manager experience

- Investment strategy

- Risk-adjusted returns

A consistently performing fund is often a better choice than one with exceptional short-term performance.

5. Investing Without a Financial Goal

Investing without a clear objective often leads to poor decisions.

Instead of investing randomly, define your purpose.

Examples include:

- Retirement

- Child’s education

- Home purchase

- Marriage

- Emergency fund

- International vacation

- Wealth creation

Goal-based investing provides direction and helps determine the appropriate investment amount and time horizon.

6. Not Increasing SIP Amount

Many investors continue investing the same amount for years, even after receiving salary increments.

Increasing your SIP by 5%–10% annually can substantially increase your final corpus.

Example

Monthly SIP: ₹10,000

Annual Increase: 10%

Over 25 years, a step-up SIP can potentially generate significantly more wealth than a fixed SIP.

7. Frequently Switching Funds

Changing mutual funds every few months based on recent performance can negatively affect long-term returns.

Allow your investments sufficient time to perform.

Review your portfolio periodically, but avoid unnecessary changes unless there is a valid reason.

8. Ignoring Asset Allocation

Putting all your money into a single mutual fund category increases concentration risk.

A diversified portfolio may include:

- Large-cap funds

- Mid-cap funds

- Small-cap funds

- International funds

- Hybrid funds

- Debt funds

Diversification can help reduce overall portfolio risk.

9. Not Reviewing Investments

Although SIPs are designed for long-term investing, they should not be ignored indefinitely.

Review your investments at least once a year.

During the review, consider:

- Fund performance

- Goal progress

- Asset allocation

- Changes in income

- Changes in financial objectives

Periodic reviews help ensure that your portfolio remains aligned with your goals.

10. Investing Beyond Your Financial Capacity

Your SIP amount should fit comfortably within your monthly budget.

Avoid investing so much that you struggle to meet essential expenses or maintain an emergency fund.

A sustainable investment plan is easier to continue over the long term.

How to Maximize SIP Returns

While no strategy can guarantee higher returns, certain practices can improve your long-term investment experience and help you make the most of compounding.

Start Early

Time is one of the most powerful factors in investing.

Starting early gives your investments more years to compound and recover from temporary market downturns.

Stay Invested for the Long Term

Historically, longer investment periods have generally reduced the impact of short-term market volatility.

Avoid redeeming investments prematurely unless required for your financial goals.

Increase SIP Every Year

As your income grows, increase your monthly investment.

Even a small annual increase can significantly improve your final corpus.

Suggested Annual Step-Up

| Salary Increase | Suggested SIP Increase |

|---|---|

| 5% | 5% |

| 10% | 10% |

| 15% | 12–15% |

Invest Consistently

Skipping SIP installments reduces the benefits of compounding.

Maintain consistency, even during market corrections.

Diversify Across Fund Categories

A balanced portfolio might include:

| Fund Type | Suggested Allocation* |

|---|---|

| Large Cap | 30–40% |

| Flexi Cap | 20–30% |

| Mid Cap | 15–20% |

| Small Cap | 10–15% |

| Hybrid/Debt | 10–20% |

*Illustrative allocation only. Actual allocation should reflect your goals, investment horizon, and risk tolerance.

Reinvest Gains

Instead of withdrawing profits frequently, consider remaining invested if the money is not immediately needed.

Allowing gains to compound can increase long-term wealth.

Avoid Emotional Investing

Market movements often trigger emotional decisions.

Common emotional mistakes include:

- Selling during market declines.

- Buying after sharp rallies.

- Following investment tips without research.

- Comparing your portfolio with others.

Successful investors generally follow a disciplined investment plan rather than reacting to short-term market events.

Keep Investment Costs Low

Expense ratios and transaction costs affect net returns.

When comparing similar mutual funds, lower expenses can contribute positively over long investment periods.

Maintain an Emergency Fund

Before investing aggressively in equity mutual funds, maintain an emergency fund covering approximately 6–12 months of essential expenses.

This reduces the likelihood of redeeming long-term investments during unexpected financial situations.

Review but Don’t Overreact

A yearly portfolio review is usually sufficient for most long-term investors.

Avoid making decisions based solely on short-term performance.

Advanced SIP Strategies

Experienced investors sometimes use advanced strategies to optimize their investment plans.

Step-Up SIP Strategy

Increase your SIP every year as your salary increases.

Example:

| Year | Monthly SIP |

|---|---|

| Year 1 | ₹10,000 |

| Year 2 | ₹11,000 |

| Year 3 | ₹12,100 |

| Year 4 | ₹13,310 |

| Year 5 | ₹14,641 |

This gradual increase can substantially enhance long-term wealth creation.

Goal-Based SIP Strategy

Instead of investing a random amount, calculate the SIP required for each financial goal.

For example:

| Goal | Target Amount | Time |

|---|---|---|

| Retirement | ₹5 Crore | 30 Years |

| Child Education | ₹40 Lakhs | 15 Years |

| Home Down Payment | ₹30 Lakhs | 10 Years |

Using separate SIPs for each goal can make tracking progress easier.

Core and Satellite Strategy

This approach combines stability with growth potential.

Example:

Core Portfolio

- Large Cap Fund

- Index Fund

- Flexi Cap Fund

Satellite Portfolio

- Mid Cap Fund

- Small Cap Fund

- International Fund

The core portfolio provides stability, while the satellite portfolio seeks additional growth.

Value Averaging Strategy

Unlike a fixed SIP, value averaging adjusts the investment amount based on market movements.

- Invest more when markets fall.

- Invest less when markets rise.

This strategy may appeal to experienced investors but requires regular monitoring and discipline.

SIP During Market Crashes

Many investors ask whether they should stop investing during a market crash.

Historically, continuing SIPs during market downturns has allowed investors to accumulate more units at lower prices, potentially improving long-term outcomes when markets recover.

Rather than viewing market declines as a reason to stop investing, long-term investors often see them as opportunities to continue building their portfolios at relatively lower valuations.

Frequently Asked Questions (FAQs)

A Systematic Investment Plan (SIP) is a method of investing a fixed amount regularly in a mutual fund instead of making a one-time investment. It helps investors build wealth gradually through disciplined investing and the power of compounding.

A SIP Calculator is an online tool that estimates the future value of your monthly investments based on your SIP amount, expected annual return, and investment period.

A SIP Calculator provides estimated results based on the assumptions you enter. Actual returns may vary depending on market performance, fund selection, and investment duration.

No. SIP is only a method of investing. Since mutual funds are market-linked investments, returns are not guaranteed.

Many mutual funds allow investors to start SIPs from as little as ₹100 or ₹500, depending on the fund house.

Yes. Most mutual funds allow you to start a new SIP with a higher amount or use a Step-Up SIP feature to automatically increase your investments.

Yes. In most open-ended mutual fund schemes, you can stop or pause your SIP without any penalty.

Missing one installment generally does not cancel your SIP. However, repeated missed payments may result in the SIP mandate being discontinued by the fund house.

Both have advantages. SIP is generally suitable for regular investors and helps reduce market timing risk, while Lumpsum investing may be appropriate if you have a large amount available and a long investment horizon.

SIPs have the potential to generate higher long-term returns but involve market risk. Fixed Deposits offer stable returns with lower risk.

Historically, equity-oriented SIPs have often generated returns that exceeded inflation over long periods, although future performance cannot be guaranteed.

Yes. SIP is one of the simplest investment methods for beginners because it encourages regular investing and reduces the need to time the market.

Yes. Many mutual fund companies allow Non-Resident Indians (NRIs) to invest through SIPs, subject to applicable regulations and documentation requirements.

Generally, an investment horizon of at least 7–10 years is considered suitable for equity mutual funds. Longer durations allow compounding to work more effectively.

Yes. You can invest in multiple mutual fund schemes simultaneously based on your financial goals and asset allocation.

The required SIP depends on your investment horizon and assumed rate of return. Our SIP Calculator helps estimate the monthly investment needed to reach your target.

Taxation depends on the type of mutual fund and the applicable tax laws in your country. Investors should review the latest tax rules or consult a qualified tax professional.

NAV (Net Asset Value) represents the per-unit value of a mutual fund and changes daily based on the fund’s underlying assets.

Most open-ended mutual funds allow redemptions at any time, although exit loads or lock-in periods may apply in certain cases, such as ELSS funds.

Continuing your SIP during market corrections allows you to purchase more units at lower prices, which may improve long-term returns when markets recover.

Investment Glossary

Understanding financial terminology helps investors make more informed decisions. Below are some commonly used investment terms.

SIP (Systematic Investment Plan)

A method of investing a fixed amount at regular intervals into mutual funds.

Mutual Fund

A professionally managed investment vehicle that pools money from multiple investors and invests it in securities such as stocks, bonds, or other assets.

NAV (Net Asset Value)

The price per unit of a mutual fund, calculated daily based on the value of the fund’s assets minus liabilities.

AMC (Asset Management Company)

A company that manages mutual funds and makes investment decisions on behalf of investors.

Expense Ratio

The annual fee charged by a mutual fund for managing the investment portfolio.

Exit Load

A fee charged by some mutual funds when investors redeem their units before a specified holding period.

Equity Fund

A mutual fund that primarily invests in shares of listed companies.

Debt Fund

A mutual fund that invests mainly in fixed-income securities such as government bonds and corporate bonds.

Hybrid Fund

A mutual fund that combines equity and debt investments within the same portfolio.

Large Cap Fund

A fund investing primarily in large, well-established companies.

Mid Cap Fund

A fund investing mainly in medium-sized companies with growth potential.

Small Cap Fund

A fund investing in smaller companies, generally associated with higher growth potential and higher risk.

ELSS

An Equity Linked Savings Scheme offering potential tax benefits under applicable tax laws along with market-linked returns.

CAGR

Compound Annual Growth Rate, representing the average annual growth rate of an investment over a specified period.

XIRR

Extended Internal Rate of Return, commonly used to calculate returns when investments are made at different dates, such as through SIPs.

Asset Allocation

The process of distributing investments across different asset classes such as equity, debt, gold, and cash to balance risk and return.

Diversification

Spreading investments across multiple assets or sectors to reduce overall portfolio risk.

Portfolio

The collection of all investments owned by an investor.

Bull Market

A period during which financial markets experience sustained price increases.

Bear Market

A period characterized by prolonged declines in market prices.

Inflation

The gradual increase in the prices of goods and services over time, reducing the purchasing power of money.

Compounding

The process where investment returns generate additional returns over time, leading to exponential growth.

Rupee Cost Averaging

A strategy where investing a fixed amount regularly results in purchasing more units when prices are low and fewer units when prices are high, helping average the purchase cost over time.

Expert Tips for Successful SIP Investing

- Start investing as early as possible.

- Stay invested for the long term.

- Increase your SIP every year through a Step-Up SIP.

- Diversify across different mutual fund categories.

- Avoid stopping SIPs during market corrections.

- Review your portfolio annually.

- Invest with specific financial goals in mind.

- Maintain an emergency fund separately from your investments.

- Avoid chasing recent top-performing funds.

- Keep a long-term perspective and avoid emotional decisions.

Key Takeaways

- SIP is one of the most effective ways to build long-term wealth.

- Consistency is more important than trying to time the market.

- The power of compounding increases significantly over longer investment periods.

- Rupee cost averaging helps manage market volatility.

- Step-Up SIPs can substantially increase your final corpus.

- Diversification helps reduce investment risk.

- Goal-based investing provides clarity and discipline.

- Regular portfolio reviews ensure your investments remain aligned with your objectives.

Conclusion

A Systematic Investment Plan is more than just a way to invest in mutual funds—it is a disciplined approach to building long-term financial security. Whether your goal is retirement, your child’s education, purchasing a home, or achieving financial independence, regular investing combined with patience and the power of compounding can help you move closer to your objectives.

Our free SIP Calculator simplifies financial planning by instantly estimating your investment growth based on your monthly contribution, expected return, and investment period. With support for multiple currencies and both SIP and Lumpsum calculations, it provides a convenient way to compare different investment scenarios and make informed decisions.

Remember that investing is a long-term journey. Staying consistent, reviewing your portfolio periodically, and aligning your investments with your financial goals can significantly improve your chances of building sustainable wealth over time.